Opening Keynote Address by Datuk Syed Zaid Albar, Chairman SC Malaysia at ESG Corporate Summit.

Scams have been increasing in the Malaysian capital market over the past few years, amid the Securities Commission’s (SC) efforts to clamp down on unscrupulous activities.

`

Chairman Datuk Syed Zaid Albar said that complaints on unlicensed schemes in 2021 had increased to 52% of total complaints received by the SC, up from 37% in 2020.

`

“In line with this, we have also stepped up our anti-scam efforts using a multi-pronged approach,” he said.

`

Syed Zaid was speaking during a virtual media briefing yesterday, following the launch of the SC’s annual report for 2021.

`

Actions taken by the SC in 2021 against unlicensed activities and unauthorised operators included issuing 24 cease and desist orders to persons carrying on unlicensed investment advice, 13 administrative sanctions via reprimands and directives, and blocking access to 143 websites via the Malaysian Communications and Multimedia Commission (MCMC).

`

To date, the SC has undertaken five enforcement actions, 473 regulatory interventions and put up 275 unlicensed companies and individuals on the SC’s Investor Alert List.

`

An internal taskforce was also established to investigate investment scams and clone firms which reviewed 159 bank accounts that identified 32 persons of interest.

`

In 2021, the SC concluded 22 investigations, and more than 55% of completed investigations last year relate to unlicensed activity and securities fraud.

`

Corporate misconduct, which constituted 14% of the total completed investigations, included disclosure breaches relating to securities laws.

`

As of Dec 31, 2021, the total number of active investigations were 46.

`

“While the SC continued to dedicate substantial resources to conduct investigations relating to securities fraud and market manipulation offences, investigations on corporate misconduct has emerged as the second highest percentage of active investigations carried out in 2021,” the commission said in the annual report.

`

Through its civil enforcement actions, the SC had in 2021 restituted RM2.7mil to a total of 721 investors who had suffered losses as a result of such breaches.

`

On a separate matter, Syed Zaid said that the SC was monitoring the issuance of non-fungible tokens (NFTs) on a case-by-case basis, amid the global craze to convert real-world items into digital assets.

`

This was, however, subject to the nature of the NFTs, the NFT projects as well as the activities carried out at the NFT marketplace, he added.

`

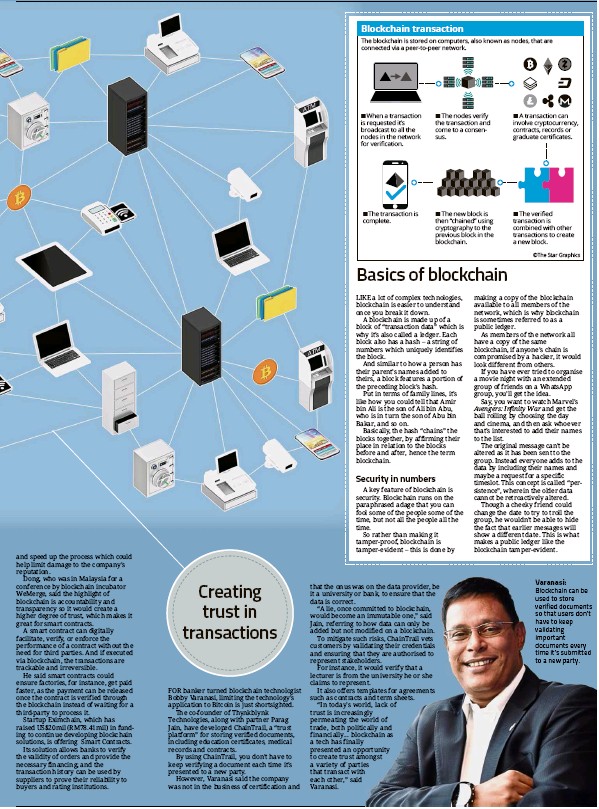

An NFT is a unique digital asset that represents ownership of real-world items like photos, videos and audios. It is a non-interchangeable unit of data stored on a blockchain, a form of digital ledger, that can be sold and traded.

`

Syed Zaid pointed out that the underlying assets of most NFTs in Malaysia were non-securities products, hence such NFTs did not fall under the SC’s regulations.

`

However, SC managing director Foo Lee Mei said that some NFTs may come under the SC’s purview, if the NFTs met the SC’s digital asset prescription order.

`

In addition, in the event any of the NFT players engaged in capital market-regulated activities, the issued NFTs would have to adhere to the SC’s rules.

`

Based on the SC’s latest annual report, Malaysia’s digital asset market continued to expand in 2021 despite the market uncertainties, with approximately RM21bil in digital assets traded across all registered digital asset exchanges (DAXs).

`

The total number of investment accounts surged by nearly 300% to about 760,000 from more than 190,000 in 2020.

Since introducing the DAX framework in 2019, the SC had registered four DAXs, namely Luno Malaysia Sdn Bhd, SINEGY Technologies (M) Sdn Bhd, Tokenize Technology (M) Sdn Bhd and MX Global Sdn Bhd.

`

Commenting on the Malaysian capital market outlook for 2022, Syed Zaid said volatility will remain, especially in the near term.

`

The outlook, he added, will be premised on the baseline expectation of a sustained economic recovery this year.

`

However, he warned that further escalation of the Russia-Ukraine conflict could disrupt the much-need economic recovery.

`

“As we have witnessed, the impacts are already felt in various market segments worldwide, especially in commodities.

“The possibility of a more severe impact still remains, given the potential for further escalation and the lack of a clear resolution.

`

“For the moment, the direct impact to Malaysia is still manageable, given our minimal exposure to Ukraine and Russia,” he said.

`

Challenges aside, Syed Zaid said the SC’s priorities in 2022 aim to shift the capital market to a relevant, efficient, diversified and inclusive ecosystem.

`

This would allow Malaysia’s national growth pillars to achieve its ambitions in areas such as digital, carbon-neutrality and managing the transition of the country into an aged nation.

`

“From an organisation perspective, the SC will strengthen its internal digital capabilities and skills set to enable the SC’s workforce to harness state-of-the art digital technology for deeper insights and engender efficiency in our risk management, surveillance and supervision functions.

`

“The SC has also embarked on its own journey towards reducing its carbon and environmental footprint, in line with Malaysia’s goal of becoming a carbon-neutral country by 2050,” he said.

`

On expected fundraising activities, Syed Zaid painted a positive outlook, underpinned by normalising economic conditions.

`

For 2022, he expects about 35 initial public offerings (IPOs) to take place.

`

In comparison, there were 29 new listings in 2021, of which six were on the Main Market, 11 were the ACE Market, and the remaining 12 were the LEAP Market. The total amount of funds raised from these new listings was approximately RM2.3bil.

`

The SC noted in its annual report that it had also considered an IPO application on the Main Market last year, which would have raised about RM4.7bil. However, the application was subsequently withdrawn.

`

“We have also received enquiries and statements of interest in SPACs (special purpose acquisition companies), but it is still too early to tell whether any SPACs will be listed in 2022,” he added.

Related posts:

Financial literacy and technology are key factors, will attract young investors

Related:

Cybersecurity Watch: How Protected Is Your Organisation?

Call to control related-party transactions | The Star

https://www.thestar.com.my/business/business-news/2022/03/29/call-to-control--related-party-transactions

Youth more aware of non-capital market products | The Star

Financial literacy tools a key factor | The Star

Core Competencies Framework on Financial Literacy for Youth

https://www.oecd.org › finance › Core-Competen...

YOUTH AS A SMART INVESTMENT - the United Nations