http://www.thestar.com.my/business/business-news/2016/05/21/fintech-disruptive-technology/

Businesses are embracing it by coming up with their innovations and startups

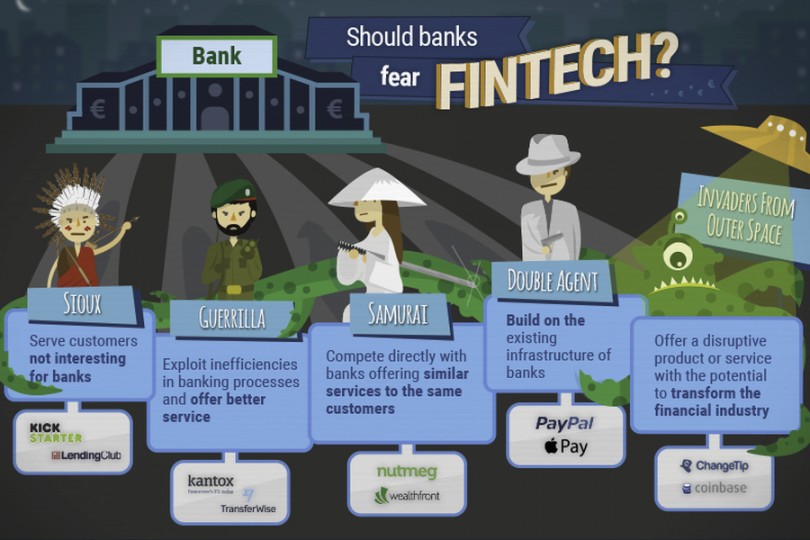

A BUZZWORD growing in popularity in the financial world today is “fintech”, short for financial technology, which in a nutshell refers to the use of technology to deliver faster and cheaper financial services.

Going by some predications, fintech could take a big chunk of business away from traditional banks as it is being run by smaller more nimble start-ups. But the debate is still out there as to how much that chunk will be. In Malaysia in particular, fintech’s presence is still nascent and small. Fintech transactions totalled a mere US$6.37mil this year compared with a global figure of US$769.3bil, according to Statista, an online statistics provider.

It however predicts that fintech transaction values to grow to US$14.4bil by 2020. A significant number of fintech companies, especially those in the digital payments space, actually work alongside local banks.

Still, fintech is not to be taken lightly. Top bankers themselves are speaking of its imminent threat to their business. Former Barclays CEO Anthony Jenkins referred to it as banking’s “Uber moment” to describe technological advances that could see bank branches close down and people laid off.

Last April, Jamie Dimon the CEO of the US’ largest bank JP Morgan in his letter to shareholders warned that “Silicon Valley is coming.” “There are hundreds of start-ups with a lot of brains and money working on various alternatives to traditional banking,” Dimon wrote.

On the home front, just last month prominent banker Datuk Seri Nazir Razak echoed such views. Speaking at the Star Media Group’s PowerTalk: Business Series held at Menara Star, Nazir opined that fintech companies are disrupting banking.

“Bankers must respond to this Uber moment. People actually dislike banks today, since the global financial crisis. Recent data suggests that in the US, the cost of banking intermediation has not changed for 100 years in real terms. This simply means banks have not gotten more efficient over the years, so its right that banks get attacked by ‘Silicon Valley’, which has identified banking as an industry that is very ‘ripe’ or juicy to disrupt.”

Even the central bank is echoing these views.

In his maiden keynote address at an Islamic finance conference in Kuala Lumpur last week, Malaysia’s newly-appointed Bank Negara governor Datuk Muhammad Ibrahim gave a grim reminder to banks of the threats posed by fintech. In particular, Muhammad quoted from a report by McKinsey that 10% to 40% of banking revenue is possibly at risk by 2025 due to innovations outside banking institutions that are able to offer a significant pricing advantage and that technologically-driven applications had spread to nearly every segment of the financial sector, with the number of fintech start-ups having doubled in the last year. “Fintech is challenging the status quo of the financial industry,” he said.

To be fair, Malaysian banks are quick to point out that while fintech does represent a disruption to business, they are embracing the movement, by coming up with their own fintech innovations or by working with fintech startups.

So what is fintech?

In a nutshell, fintech is an economy of companies using technology to improve efficiencies and effectiveness in the financial services industry. To illustrate the offerings of fintech companies, consider the business model of homegrown start-up MoneyMatch, which is modelled after UK-based TransferWise which began in 2011 and today moves US$10bil a year through its platform.

MoneyMatch has created a platform to match individual buyers and sellers of currencies, with the attraction of both sides enjoying better exchange rates than what banks and even money changers offer. The rate used by the MoneyMatch site is the middle rate of the currency exchange spread. So an individual for example, willing to buy US$100 for his travels will be matched with someone wanting to change his US$100 into ringgit. The parties will be matched on this application and then proceed to make their exchange in an agreed location. MoneyMatch is also entering the area of cross border fund transfers.

“For example, someone in Singapore wishing to transfer money to Malaysia can be matched with someone here wishing to send an equal amount of money across the Causeway. Hence the parties can make the respective transfers to local accounts of their choice after an exchange of information. This means the transfer is done minus any cross-border transfer fees,” explains MoneyMatch co-founder Naysan Munusamy, who had spent many years as a forex trader with a number of banks before venturing out to start MoneyMatch.

Peer lending

One key growth area in fintech is peer to peer or P2P lending, online platforms that match borrowers with lenders, bypassing the traditional financial institutions. The business had even attracted big names such as Goldman Sachs. The most notable name in this space is Lending Club, which had launched its service as far back as 2007 and became the US’ largest technology IPO in 2014, raising around US$1bil.

Lending Club claims that its platform – which enables borrowers to get unsecured loans of US$1,000 to US$35,000 – has now helped originate close to US$16bil in loans.

Locally, last month the Securities Commission (SC) launched a regulatory framework for P2P lending, paving the way for small and medium-sized companies to access this new avenue of debt funding. Under SC’s rules though, individuals are not allowed to raise money on the local P2P platforms. Rather it is meant to only fund projects and businesses and a number of safeguards are in place. For example, those behind the operator of the P2P platform need to pass the “fit and proper” test; the rate of financing cannot be more than 18% (as that would be deemed predatory lending) and that the P2P operator has to disclose information related to the issuer and the risk assessment and credit scoring parameters adopted by the operator. There is no authorized P2P platform in Malaysia yet as parties wishing to run such platforms have to submit their application to the SC soon.

In China, P2P lending has virtually exploded. As a recent report by Citibank highlights, “China is past the tipping point”, with fintech companies having similar number of clients as the major banks. The report notes that China is the largest P2P lender in the world, with transactions topping US$66bil, compared with the US with only US$16.6bil.

Regulating fintech

But there are problems. Some unregulated P2P platforms in China had run scams. Others helped fuel an equity roller-coaster by offering funding for stock investments. This led to the Chinese benchmark index rallying more than 150% in the 12 months to last June before abruptly crashing. The Chinese authorities are now cleaning up the P2P sector.

So what are the risks of fintech regulation in Malaysia? And do companies like MoneyMatch need be regulated and licensed?

In an emailed reply to StarBizWeek, Bank Negara says: “Fintech start-ups that engage in activities under the purview of the central bank must comply with existing laws”. Bank Negara explains that regulated businesses include banking, insurance or takaful, money changing, remittance, operating a payment system or issuing payment instruments.

“A fintech company that engages in any activity that falls within the definition of a regulated business must be properly authorised to do so under the relevant laws.

“As an example, collecting deposits via a fintech platform would require approval from Bank Negara.

“A fintech company that is authorised to conduct a regulated business under the laws that Bank Negara administers will be subject to the oversight of Bank Negara pursuant to those laws.”

What this indicates is that Bank Negara is going to regulate fintechs the same way it does banks. But exactly how, it still isn’t clear.

But the good news is this: Bank Negara says it is engaging with firms in this space (and presumably that includes the likes of MoneyMatch), “to understand and where appropriate facilitate their business and provide guidance on aspects on regulation that would be applicable to them.”

Bank Negara adds that it is in the process of formulating a framework that “encourages innovation without undermining financial stability, the integrity of the financial system or the adequate protection for financial consumers.”

The SC has also been pushing for fintech innovation to develop in Malaysia. Last year, Malaysia became the first country in the region to introduce the regulatory framework for equity crowd funding. (While P2P is about companies raising debt, crowd funding is for entrepreneurs to sell equity to investors.)

The SC has also launched aFINity@SC, a fintech community aimed at industry engagement and more recently launched the P2P financing framework, which is aimed at addressing the funding needs of small businesses.

Chin Wei Min, the SC’s new head of innovation and digital strategy, says: “We think fintech can provide solutions to some of the unserved and underserved needs in the capital market.”

Chin adds: “We are also mindful of the risk, fraud and all the pitfalls. We continue to enhance our engagement model. We want to remain very close to the industry.”

Fintech’s hiccups

Some recent developments in the fintech space, however, point to weaknesses in fintech companies. LendingClub, the poster boy company for P2P lending has seen its shares tumble, wiping out about a third of its market value.

This came as it faces scrutiny after its founder and CEO resigned following an investigation into improper loan sales.

The US Treasury has released a report criticising the P2P lending business, recommending it to be more tightly regulated. Some commentators are liking P2P lending to the early days of the subprime mortgage bubble of 2006-07.

It is more likely though that the experiences of fintech in mature markets like China and the US will serve as good guides as to how this business will grow in this part of the world, with the requisite regulations put in place.

And the jury is still out as to whether traditional banks here will lose significant parts of their businesses to fintech start-ups.

Or as one industry observer puts it, fintech is more likely to usurp the business of the shadow banking market here, as some unserved borrowers now have the option to move away from loan sharks or “Ah Longs” and into the crowd funding or P2P platforms. But after that, banks could be next.

By Risen Jayaseelan, Wong Wei-Shen, a Zunaira Saieed The Star

Related story:

Banking on fintech

Banking on fintech

Related post:

Apr 16, 2016 ... WHO dominates the phone dominates the Internet. The whole world of

information is now available in your hand, replacing your own mind as a ...

The Bank of England in the City of London.

The Bank of England in the City of London.

{kind=link}